IC Insights recently released its September Update to the 2016 McClean Report. This Update included Part 2 of an extensive analysis of the IC foundry industry and a look at the current state of the merger and acquisition surge in the semiconductor industry. An excerpt from the M&A portion of this Update is shown below.

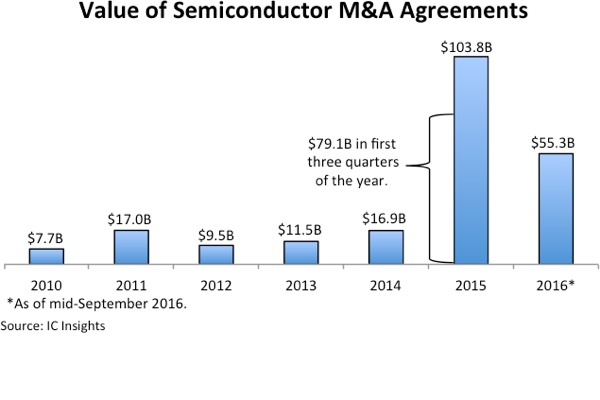

After an historic surge in semiconductor merger and acquisition agreements in 2015, the torrid pace of transactions has eased (until recently), but 2016 is already the second-largest year ever for chip industry M&A announcements, thanks to three major deals struck in 3Q16 that have a combined total value of $51.0 billion. As of the middle of September, announced semiconductor acquisition agreements this year have a combined value of $55.3 billion compared to the all-time high of $103.8 billion reached in all of 2015 (Figure 1). Through the first three quarters of 2015, semiconductor acquisition pacts had a combined value of about $79.1 billion, which is 43% higher than the total of the purchasing agreements reached in the same period of 2016, based on M&A data compiled by IC Insights.

In many ways, 2016 has become a sequel to the M&A mania that erupted in 2015, when semiconductor acquisitions accelerated because a growing number of suppliers turned to purchase agreements to offset slower growth in major existing end-use equipment applications (such as smartphones, PCs, and tablets) and to broaden their businesses to serve huge new market potentials, including the Internet of Things (IoT), wearable electronics, and strong segments in embedded electronics, like highly-automated automotive systems. China’s goal of boosting its domestic IC industry is also driving M&A. In the first half of 2016, it appeared the enormous wave of semiconductor acquisitions in 2015 had subsided substantially, with the value of transactions announced between January and June being just $4.3 billion compared to $72.6 billion in the same six-month period in 1H15. However, three large acquisition agreements announced in 3Q16, including SoftBank’s purchase of ARM, Analog Devices’ intended purchase of Linear Technology, and Renesas’ potential acquisition of Intersil) have insured that 2016 will be second only to 2015 in terms of the total value of announced semiconductor M&A transactions.

A major difference between the huge wave of semiconductor acquisitions in 2015 and the nearly 20 deals being struck in 2016 is that a significant number of transactions this year are for parts of businesses, divisions, product lines, technologies, or certain assets of companies. This year has seen a surge in the agreements in which semiconductor companies are divesting or filling out product lines and technologies for newly honed strategies in the second half of this decade.

Report Details: The 2016 McClean Report