Record annual ASP growth rates forecast for both memory segments.

In its upcoming Mid-Year Update to The McClean Report 2017 (to be released at the end of July), IC Insights addresses the amazing growth of the 2017 DRAM and NAND flash memory markets.

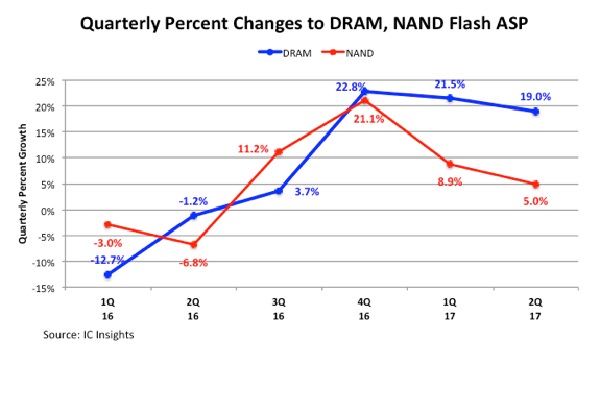

Sales of both memory types—DRAM and NAND—are expected to set record highs this year. In both cases, the strong annual upturn in sales is being driven almost entirely by fast-rising average selling prices. In the case of DRAM, unit shipments are actually forecast to show a decline this year. Moreover, NAND shipments are forecast to increase only 2%, providing a small, added boost to the market growth in that segment. Prices for DRAM and NAND first began increasing in the second half of 2016, and continued with quarterly increases through the first half of 2017. Figure 1 plots the robust quarterly ASP growth rates, which, from 3Q16 through 2Q17, averaged 16.8% for DRAM and 11.6% for NAND.

With DRAM ASPs surging since the third quarter of 2016, DRAM manufacturers once again stepped up their spending for this segment. However, the majority of this spending is going towards technology advancements and not toward capacity additions.

IC Insights believes that essentially all of the spending for flash memory in 2017 will be used for 3D NAND flash memory process technology as opposed to planar flash memory. A big increase in NAND flash capital spending this year is expected from Samsung as it ramps 3D NAND production at its large, new fab in Pyeongtaek, South Korea.

Historical precedent in the memory market shows that too much spending usually leads to overcapacity and subsequent pricing weakness. Samsung, SK Hynix, Micron, Intel, Toshiba/SanDisk, and XMC/Yangtze River Storage Technology each plan to significantly ramp up 3D NAND flash capacity over the next couple of years (with additional new Chinese producers possibly entering the market). The likelihood of overshooting 3D NAND flash capacity over the next few years is very high.

IC Insights shows the DRAM quarterly ASP growth rate peaked in 4Q16 but continued a strong upward trend through 2Q17. IC Insights forecasts the DRAM ASP to increase (though marginally) into 3Q17 before edging slightly negative in 4Q17, signaling the end of another cyclical upturn.

Even though DRAM ASP growth is forecast to slow in the second half of the year, the annual DRAM ASP growth rate is still forecast to be 63%, which would be the largest annual rise for DRAM ASPs dating back to 1993 when IC Insights first started tracking this data. The previous record-high annual growth rate for DRAM ASP was 57% in 1997. For NAND flash, the 2017 ASP is forecast to increase 33%, also a record high gain. (In the year 2000, the predominantly NOR-based flash ASP jumped 52%).

The 250+ page Mid-Year Update to the 2017 edition of The McClean Report further describes IC Insights’ updated forecasts for DRAM and NAND flash memory for 2017-2021 and includes a refreshed outlook on its semiconductor capital expenditure forecast.

Report Details: The 2017 McClean Report

Additional details on the IC market forecast and other trends within the IC industry are provided in The McClean Report—A Complete Analysis and Forecast of the Integrated Circuit Industry (released in January 2017). A subscription to The McClean Report includes free monthly updates from March through November (including a 250+ page Mid-Year Update), and free access to subscriber-only webinars throughout the year. An individual-user license to the 2017 edition of The McClean Report is priced at $4,090 and includes an Internet access password. A multi-user worldwide corporate license is available for $7,090.