Skyrocketing DRAM prices potentially open the door for startup Chinese competitors.

Historically, the DRAM market has been the most volatile of the major IC product segments. A good example of this was displayed over the past two years when the DRAM market declined 8% in 2016 only to surge by 77% in 2017! The March Update to the 2018 McClean Report (to be released later this month) will fully detail IC Insights’ latest forecast for the 2018 DRAM and total IC markets.

In the 34-year period from 1978-2012, the DRAM price-per-bit declined by an average annual rate of 33%. However, from 2012 through 2017, the average DRAM price-per-bit decline was only 3% per year. Moreover, the 47% full-year 2017 jump in the price-per-bit of DRAM was the largest annual increase since 1978, surpassing the previous high of 45% registered 30 years ago in 1988!

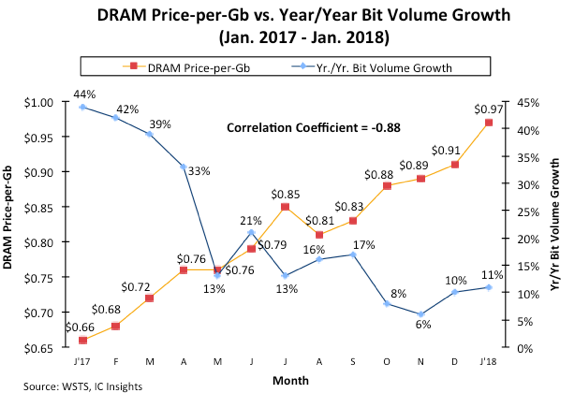

In 2017, DRAM bit volume growth was 20%, half the 40% rate of increase registered in 2016. For 2018, each of the three major DRAM producers (e.g., Samsung, SK Hynix, and Micron) have stated that they expect DRAM bit volume growth to once again be about 20%. However, as shown in Figure 1, monthly year-over-year DRAM bit volume growth averaged only 13% over the nine-month period of May 2017 through January 2018.

Figure 1 also plots the monthly price-per-Gb of DRAM from January of 2017 through January of 2018. As shown, the DRAM price-per-Gb has been on a steep rise, with prices being 47% higher in January 2018 as compared to one year earlier in January 2017. There is little doubt that electronic system manufacturers are currently scrambling to adjust and adapt to the skyrocketing cost of memory.

DRAM is usually considered a commodity like oil. Like most commodities, there is elasticity of demand associated with the product. For example, when oil prices are low, many consumers purchase big SUVs, with little concern for the vehicle’s miles-per-gallon efficiency. However, when oil prices are high, consumers typically look toward smaller or alternative energy (e.g., hybrid or fully electric) options.

Figure 1

While difficult to precisely measure, it is IC Insights’ opinion that DRAM bit volume usage is also affected by elasticity, whereby increased costs inhibit demand and lower costs expand usage and open up new applications. As shown in Figure 1, the correlation coefficient between the DRAM price-per-bit and the year-over-year bit volume increase from January 2017 through January 2018 was a strong -0.88 (a perfect correlation between two factors moving in the opposite direction would be -1.0). Thus, while system manufacturers are not scaling back DRAM usage in systems currently shipping, there have been numerous rumors of some smartphone producers scaling back DRAM in next-generation models (i.e., incorporating 4GB of DRAM per smartphone instead of 5GB).

In 2018, IC Insights believes that the major DRAM suppliers will be walking a fine line between making their shareholders even happier than they are right now and further alienating their customer base. If, and it is a BIG if, the startup Chinese DRAM producers can field a competitive product over the next couple of years, DRAM users could flock to these new suppliers in an attempt to get out from under the crushing price increases now being thrust upon them—with the “payback” to the current major DRAM suppliers being severe.