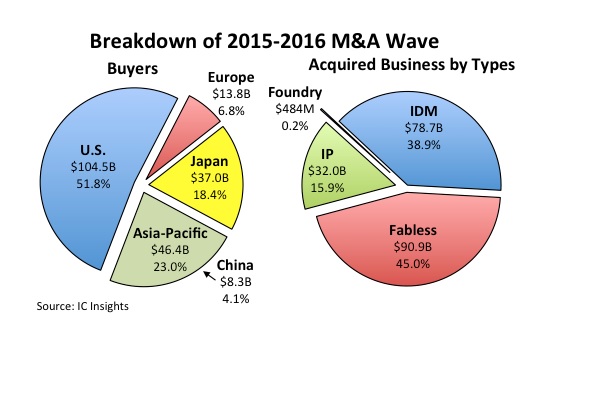

U.S. companies making acquisitions accounted for more than half of the value in announced transactions in the last two years, while Asia-Pacific represented 23%.

More than two dozen acquisition agreements were announced by semiconductor companies worldwide in 2016 with a combined value of $98.5 billion compared to the record-high $103.3 billion in purchases struck in 2015, when over 30 deals were reached, according to a summary and analysis in IC Insights’ new 2017 McClean Report. The dollar value of merger and acquisition agreements in 2015 and 2016 were both about eight times greater than the $12.6 billion annual average of M&A announcements in the five previous years (2010-2014), says the new report, which becomes available in January 2017. Nearly half of the 15 largest semiconductor acquisitions in history were announced in the 2015 2016 period, according to a ranking of M&A transactions over $2 billion in the 2017 McClean Report (Figure 1). A total of 27 semiconductor acquisition agreements have had dollar values of $2 billion or more since 1999.

Figure 1

IC Insights’ ranking and acquisition data cover semiconductor suppliers, wafer foundries, and businesses licensing intellectual property (IP) for integrated circuit designs, but excludes transactions for fab equipment and material companies, chip packaging and testing operations, and design automation firms. Overall, seven of the industry’s $2 billion-plus semiconductor acquisitions occurred in 2015 and five took place in 2016, with three each being announced in 2014, 2011, and 2006, two in 2012, and one each in 2013, 2009, 2000, and 1999.

Semiconductor M&A greatly accelerated in 2015 and continued to be high in 2016 as companies turned to acquisitions to offset slow growth in major end-use applications (such as smartphones, personal computers, and tablets). In the last two years, acquisitions have been driven by companies aiming to expand into huge new markets, especially the Internet of Things, wearable electronics, and highly intelligent embedded systems, such as automated driver-assist features in cars and autonomous vehicles in the future. China’s goal of boosting its domestic semiconductor industry has added fuel to the M&A movement.

While Chinese moves to buy foreign semiconductor suppliers and assets grabbed a great deal of attention and scrutiny by governments wanting to protect national security and industries, U.S. businesses acquiring other companies, product lines, technologies, and assets accounted for 52% of the 2015-2016 M&A value, or about $104.5 billion (Figure 2). Asia-Pacific companies were second among those making semiconductor acquisitions with 23% of the $201.5 billion two-year total, or $46.4 billion. Within the Asia-Pacific region, China represented 4% of the total, or $8.3 billion.

Figure 2 (on top) also shows a breakdown the 2015-2016 acquisition agreements by semiconductor business types with the purchase of IDMs or parts of those companies being nearly 39% of the two-year total and takeovers of fabless chip suppliers, their product lines, and/or assets representing 45%. Acquisitions of semiconductor-design intellectual property suppliers and IP assets accounted for nearly 16% of the 2015-2016 M&A value while purchase agreements for wafer-foundry businesses and assets represented just 0.2% of the total.