IC Market Drivers 2018 report ranks major end-use applications and their impact on IC market growth

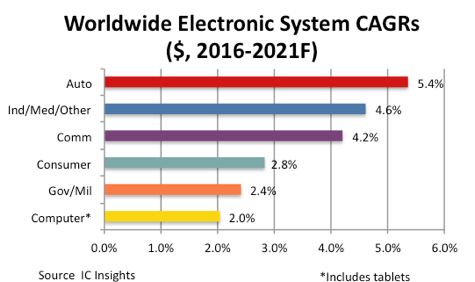

Automotive electronic system sales are forecast to rise by a compound annual growth rate (CAGR) of 5.4% from 2016 through 2021, which is the highest among six major end-use system categories (Figure 1), according to data presented in the 2018 edition of the IC Insights’ IC Market Drivers—A Study of Key System Applications Fueling Demand for Integrated Circuits that will be released later this year.

Demand is rising for electronic systems in new cars with increasing attention focused on self-driving (autonomous) vehicles, vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communications, as well as on-board safety, convenience, and environmental features, and growing interest in electric vehicles. Automotive electronics is growing as technology becomes more widely available on mid-range and entry-level cars and as consumers purchase technology-based aftermarket products. For semiconductor suppliers, this is good news as analog ICs, MCUs, and a great number of sensors are required for many of these automotive systems.

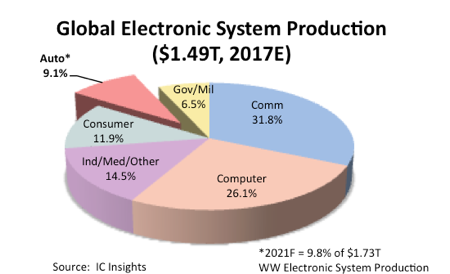

The automotive segment is expected to account for an estimated 9.1% of the $1.49 trillion total worldwide electronic systems market in 2017 (Figure 2), a slight increase from 8.9% in 2015, and 9.0% in 2016. Automotive’s share of global electronic system production has increased only incrementally through the years, and is forecast to show only marginal gains as a percent of total electronic systems market through 2021, when automotive electronics are forecast to account for 9.8% of global electronic systems sales. Though many electronics systems are being added in new vehicles, IC Insights believes pricing pressures on both ICs and electronic systems will keep the automotive end-use application from accounting for much more than its current share of total electronic systems through the forecast period.

Demand is rising for electronic systems in new cars with increasing attention focused on self-driving (autonomous) vehicles, vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communications, as well as on-board safety, convenience, and environmental features, and growing interest in electric vehicles. Automotive electronics is growing as technology becomes more widely available on mid-range and entry-level cars and as consumers purchase technology-based aftermarket products. For semiconductor suppliers, this is good news as analog ICs, MCUs, and a great number of sensors are required for many of these automotive systems.

The automotive segment is expected to account for an estimated 9.1% of the $1.49 trillion total worldwide electronic systems market in 2017 (Figure 2), a slight increase from 8.9% in 2015, and 9.0% in 2016. Automotive’s share of global electronic system production has increased only incrementally through the years, and is forecast to show only marginal gains as a percent of total electronic systems market through 2021, when automotive electronics are forecast to account for 9.8% of global electronic systems sales. Though many electronics systems are being added in new vehicles, IC Insights believes pricing pressures on both ICs and electronic systems will keep the automotive end-use application from accounting for much more than its current share of total electronic systems through the forecast period.

Candela’s largest funding round to date, with the World Bank’s IFC arm joining existing investors,…

• Charles H. Bennett helped pioneer the foundations of quantum information science alongside co-laureate Gilles…

Delta Reaches New Milestone in Electrified Intralogistics Infrastructure Delta, a global leader in power and…

First-of-its-kind framework enables seamless integration of quantum computers with advanced accelerators to support AI-native and…

The Bundeswehr acquires a fourth Automated Driverless Testing Solution from AB Dynamics The solution removes…

Munich, Germany – 17 March 2026 – Infineon Technologies AG (FSE: IFX / OTCQX: IFNNY)…

{kind=link}

{kind=link}